A期客

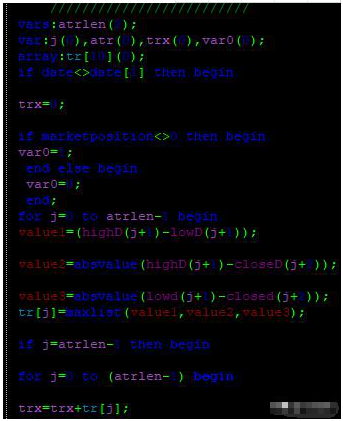

A期客经典国债期货套利量化源代码学习,适用于博易真格量化平台,大家可以下载学习。

如果有什么问题,可以直接在贴子底部回复。

# coding:utf-8

#!/usr/bin/env python

from PoboAPI import *

import datetime

import numpy as np

#债券期货价差策略,10年期国债与5年期国债价差 spread trade on 10y and 5y bond futures

def OnStart(context) :

print "I\'m starting..."

context.myacc = None

if context.accounts.has_key("回测期货"):

print "登录交易账号[回测期货]"

if context.accounts["回测期货"].Login() :

context.myacc = context.accounts["回测期货"]

SubscribeQuote(["T1812.CFFEX","TF1812.CFFEX"])

g.code1="T1812.CFFEX"

g.code2="TF1812.CFFEX"

def OnOrderChange(context, AccountName, order) :

Test = context.accounts["回测期货"].GetOrder(order.id)

print str(Test.volume)

def OnQuote(context,code) :

option=PBObj()

#option.buysellflag='0'

pos = context.accounts["回测期货"].GetPositions()

#print "positions ",pos

#print "len(pos) ",len(pos)

leg1 = GetQuote(g.code1)

leg2 = GetQuote(g.code2)

leg1now=leg1.now

leg2now=leg2.now

spreadnow=leg1now-leg2now

print "spread "+str(spreadnow) # 最新价差

if spreadnow<=0.5 and len(pos)==0 : #10债和5债价差小于0.5就买10债卖5债

print "to buy Spread....要开仓"

context.myacc.InsertOrder(g.code1, BSType.BuyOpen, leg1now, 10)

context.myacc.InsertOrder(g.code2, BSType.SellOpen, leg2now, 10)

print "positions bought"

bal=context.accounts["回测期货"].AccountBalance.AssetsBalance #返回成交后账户权益

print "账户金额 :"+str(bal)

#orders = context.accounts["回测期货"].GetOrder(order.id)

#print str(orders.volume)

#OnOrderChange(context, "回测期货", order)

TradeDetails = context.accounts["回测期货"].GetTradeDetails()

print TradeDetails

#print "len(pos) in trade ",len(pos)

pos = context.accounts["回测期货"].GetPositions()

print "len(pos) str in trade "+str(len(pos))

if spreadnow>1 and len(pos)>0: #有持仓且最新价差大于1就卖出止盈

print "to sell Spread..."

context.myacc.InsertOrder(g.code1, BSType.SellClose, leg1now, 10)

context.myacc.InsertOrder(g.code2, BSType.BuyClose, leg2now, 10)

print "positions sold,已经获利平仓"

bal=context.accounts["回测期货"].AccountBalance.AssetsBalance #返回成交后账户权益

print "账户金额 :"+str(bal)

pos = context.accounts["回测期货"].GetPositions()

print "len(pos) str in trade "+str(len(pos))

if spreadnow<=0.3 and len(pos)>0: #有持仓且最新价差小于0.3就卖出止损

print "to sell Spread..."

context.myacc.InsertOrder(g.code1, BSType.SellClose, leg1now, 10)

context.myacc.InsertOrder(g.code2, BSType.BuyClose, leg2now, 10)

print "positions sold 已经止损"

bal=context.accounts["回测期货"].AccountBalance.AssetsBalance #返回成交后账户权益

print "账户金额 :"+str(bal)

pos = context.accounts["回测期货"].GetPositions()

print "len(pos) str in trade "+str(len(pos))

Click to rate this post!